When President Trump unveiled his ‘Liberation Day’ roster of trade tariffs, the S&P 500 plummeted by 10 percent in two days. It hit a low of almost 20 percent below the peak it reached mid-February.

Investors dreaded the effect of arbitrary levies on American firms whose supply chains relied on cheaply-manufactured foreign goods. Frothily-valued Silicon Valley shares suffered more than most.

Treasury Secretary Scott Bessent initially shrugged off the volatility, pointing out – quite reasonably – that a short, sharp shock today could be interpreted as a healthy ‘correction’, preferable to letting imbalances fester.

Investors were further unsettled when President Trump began to lash out at Jerome Powell, the Chairman of the Federal Reserve, insisting that he cut interest rates or start polishing his CV.

But when the cost of US government borrowing – visible in Treasury yields – reached uncomfortably high levels, Washington paused and even dialled back its plans.

American share prices have recovered as consensus builds that Great Depression-level economic self-destruction is no longer plausible, thanks to the return of bond vigilantes.

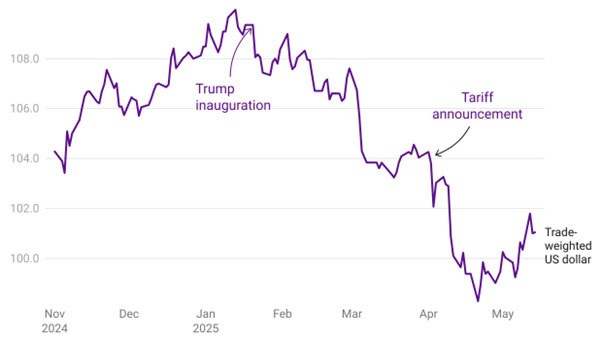

However, the dollar itself remains weakened. It is still down 5 percent against the pound, and 8% against the Swiss franc. It seems that while confidence in US enterprise has returned, confidence in the US government remains shaken.

US dollar remains weak

The dollar fell after Trump’s inauguration and on tariff announcements, and failed to recover

Chart: Weatherbys Private Bank – Created by Datawrapper

Might King Dollar lose its crown?

There has been discussion about whether the dollar could lose its status as the world’s ‘reserve currency’, and with it the privilege of US Treasuries being the ultimate safe-haven asset. The fact that the question is even being entertained says something.

Are such fears really justified? What would it take for the dollar to follow in the footsteps of the Dutch guilder, the British pound and others that were once the world’s benchmark?

First, it’s important to separate the foreign exchange rate of a currency from its ability to retain its value. A weaker dollar does not by itself imply a loss of confidence in the US. Simple market forces are usually enough to explain currency fluctuations.

For example, international investors prefer central banks that offer higher interest rates, just as we do on the high street. Indeed, monetary policy is the primary lever that policymakers pull to shore-up currencies when under threat.

Currencies are also the subject of unpredictable speculation, and indeed the vagaries of supply and demand more generally. After all, printing money – hugely expanding the supply – is well known as a sure way to depress a currency’s value.

The supply of a currency is also affected by global trade. As we import goods from abroad, we increase the international supply of pounds, which reduces their relative value. This makes imports more expensive, and so there is an element of self-correction.

But also like a high street bank, currencies can go out of favour when the national balance sheet goes awry. If growth is scant, and public spending consistently exceeds tax revenues, exchange rates will move with the eyebrows of international investors.

Is the dollar under threat in this respect?

Economic health

Companies are loath to invest when the rules of the game are uncertain, and there is already anecdotal evidence of this. For example, Microsoft paused plans to invest $1 billion in a cutting-edge AI data centre in Ohio, which would have created hundreds of local jobs.

Wider effects can also be seen in the decision by Haas Automation – a manufacturer of machine tools with links to Formula One – to reduce production at its California plant, eliminate overtime, and cease new hiring.

That said, recent economic snapshot surveys have been reassuring. The Institute of Supply Management (ISM)’s Purchasing Managers Indices (PMIs) still indicate that the US services sector is expanding, and the manufacturing sector is only contracting very slightly.

Furthermore, employment data – while somewhat backward-looking –shows little sign of trouble. US consumers are remarkably resilient, but the one thing that could stop them in their tracks is losing their jobs. Thankfully, layoff rates remain low.

Thus, the US’s still-pink economic health would suggest no imminent threat to the dollar on this front.

The federal deficit

The US’s debt to GDP ratio is currently 122 percent, having spiked after the Covid pandemic. But when you take its international assets into account, its net external debt is estimated to be just below 100 percent.

This is elevated by historical standards and uncomfortably high. However, it is not the level that is ruinous. What also matters is the rate of change. In 2024, the public deficit was an eye-watering 6.6 percent of GDP, with a projection of 6.2 percent for 2025.

Elon Musk’s Department of Governmental Efficiency (DOGE) aims to put a dent in this figure, but it’s clear that the US will either have to grow at a phenomenal clip to outrun this problem, or drastically adjust the balance of tax revenue and spending.

The sheer scale of the US’s net external debt would be enough to seriously degrade most currencies. The dollar, however, enjoys a privileged status which grants it a considerable degree of immunity.

Public spending is entirely within the gift of policymakers to curtail, should they choose to do so before heading over the brink.

But foreign holders will only take so much. Beyond a certain point, central banks with substantial dollar reserves may decide that they would be better off exchanging them for a less stressed currency. They may even decide to do it in a targeted, deliberate way, if they consider the US a geopolitical adversary. If that happened, the dollar might lose its eminence, and could fall sharply if what was once indulged was punished instead. As such, the US’s uncontrolled deficit represents a severe weak spot in the dollar’s defences.

Money supply

In recent years, central banks have slowly reduced the sizes of their swollen balance sheets, through a process of quantitative tightening (QT). In other words, the money supply is slowly shrinking.

In a vacuum, this would result in a strengthening of the dollar, because the Fed’s QT programme is more aggressive than, for example, the Bank of England’s.

As for trade flows – by themselves, tariffs on goods entering the US might reduce imports, resulting in a stronger dollar. Indeed, in the first quarter of the year, import figures were so vast that they resulted in a technical contraction in the size of the US economy.

But this was due to firms importing vast quantities of foreign goods to pre-emptively avoid tariffs – and the dollar weakened all the while.

This suggests that there is one factor which matters far more: confidence.

It all comes down to confidence

The price of gold is, among other things, a gauge of anxiety. In particular, it soars when bought in volume by those who think that the real value of a dollar is set to decline.

It is telling that gold has rocketed past the $3,000 per troy ounce mark since the start of the year. A substantial number of investors are aghast at the world’s predominant economy being captive to socialised truths.

The most dangerous thing about this episode is the possibility of an unpredictable, sudden swing in asset prices which, one way or another, sparks the kind of negative feedback loop in the dollar that briefly afflicted the pound in aftermath of Liz Truss’s ‘Mini Budget’.

But for now, the relatively modest decline in the value of the dollar so far compared to other ‘safe’ currencies suggests that the market is sensibly penalising the greenback, not writing it off entirely.

In summary, the US’s vast and growing debt pile has both exacerbated fears over the worth of its currency, while simultaneously providing the means of containing them: grumpy creditors.

And besides – if the dollar was not the world’s reserve currency, what could credibly replace it?