The phenomenon is simple enough to explain: the quantity of goods and services that money can buy shrinks over time as prices rise. In other words, the “real value” of wealth declines.

Inflation – sometimes known as the “silent thief” – is the culprit. Even a moderate increase in the cost of living can diminish purchasing power. Most incomes usually rise roughly in line with inflation, but savings can be eroded away if held as cash. The challenge is to prevent capital from dwindling.

One potential solution, of course, is to invest in assets that can keep pace with or even outstrip inflation. Yet this might involve either taking on an intolerable degree of risk or relatively complex, opaque instruments whose success is far from guaranteed.

An alternative and less widely appreciated approach is to invest in index-linked UK government bonds (known as “gilts”). In our view, these represent a prudent and potent means of preserving purchasing power, thus keeping the silent thief at bay.

What are index-linked gilts?

One reason why index-linked gilts are perhaps less recognised than they should be is that this is not necessarily an asset class that sets pulses racing. It can appear a little technical and even rather dull.

This is nothing if not ironic. The apparent lack of glamour and excitement surrounding index-linked gilts is precisely what makes them attractive in the first place. Their dependability is at the absolute heart of their appeal.

To understand why, we first need to note that UK government bonds can be broadly divided into two camps. Warning: what follows may seem slightly tedious, but it is extremely important!

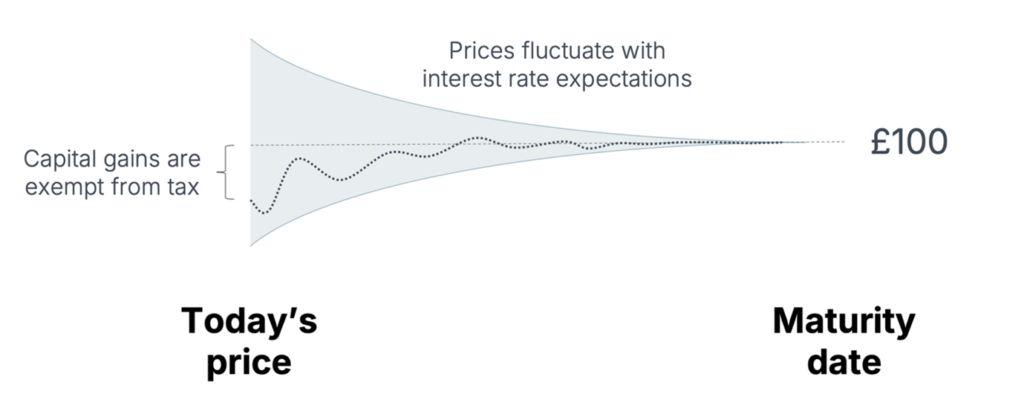

A conventional gilt is a loan to the government. It pays a fixed interest amount every six months, plus a fixed repayment at maturity. As a result, while payments are predictable, the investment as a whole is inherently susceptible to inflation risk.

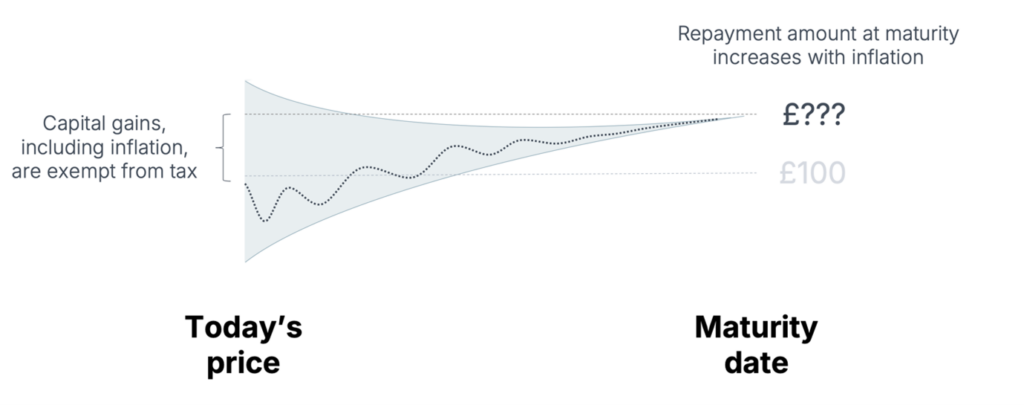

By contrast, an index-linked gilt adjusts both its periodic interest and final repayment in line with inflation. Currently the link is to the Retail Price Index (RPI), but it is set to change to the Consumer Price Index (CPI) in future.

To put it another way: while a conventional gilt’s interest and final repayment are fixed in nominal terms, for an index-linked gilt they are fixed in real terms. The illustrations below show how this might play out over time.

Conventional gilt

Index-linked gilt

A degree of certainty in an uncertain world

Given all the above, it is vital to acknowledge that the strength of index-linked gilts does not lie in their capacity to maximise returns. The objective is not to “shoot the lights out” in spectacular style, as a stock market investment might (or might not). Equities are unbeatable for their growth prospects – but it might not be necessary to take on that level of risk just to match inflation.

That said, gilts are not without risk themselves. Even when inflation spikes, index-linked gilts can temporarily decline in value if interest rates rise sharply as well. Investors should be prepared to ride out short-term volatility and hold until maturity.

The key attribute here is reassurance. Not least against a backdrop of significant geopolitical and economic uncertainty, index-linked gilts can offer a welcome source of equanimity when it comes to preserving long-term real value.

And now that index-linked gilts offer real returns comparable to those you might expect from a traditional low-to-medium-risk portfolio, it is well worth asking the question of which is better suited to meeting long-term financial objectives.

In our opinion, individuals nearing or in retirement; families with future funding obligations; and trustees, estates and other entities facing long-term planning scenarios could seriously consider whether index-linked gilts have a role to play. For example, buying a series of them maturing one year after another could be a canny way to construct an inflation-linked sequence of future inflows

In summary, inflation lives up to its “silent thief” tag by eroding purchasing power quietly in the background – but index-linked gilts can thwart it in much the same vein. We will always advocate for clients to achieve their goals in a less risky way if at all possible, and right now index-linked gilts could offer an attractive opportunity in this regard.

Start a conversation with us about index-linked gilts

We will start by understanding the level of income you may require each year to support your spending in later life. We can then look at how best to invest your assets to provide a regular flow of payments to meet those needs.

What you need to know

We advise on investments in UK gilts only as part of the Weatherbys Investment and Wealth Advice service. This can take the form of an ongoing advisory service, or a one-off consultation

The value of gilts can go down as well as up and you may not get back what you originally invested, especially if you sell before the maturity date.

Index-linked gilts may still lose value when inflation increases if interest rates rise too. Bond prices decline as market expectations of future interest rates increase.

Yields will fluctuate and therefore differ from the illustrative yields shown. Longer dated gilts are more sensitive to changes in interest rates.