Key points:

- 1970s-style stagflation will not happen

- This is stagflation ‘lite’ – short-lived and not severe

- Interest rates will rise – but only gradually and slowly

- Equity markets will be uncertain in the short term before rising again next year

What is stagflation?

Stagflation occurs when weak or declining economic activity combines with a sustained period of rising prices. The last time the UK encountered a big bout of stagflation was in the 1970s, when oil prices rose steeply in 1973 and then again in 1979 pushing up inflation and triggering recessions.

What is the evidence pointing to stagflation now?

We are ticking both boxes. First, inflation is rising. In August, inflation was 3.2%, a nine-year high. And we expect inflation to continue to rise for several reasons, such as the surge in wholesale gas prices. We expect inflation to be 4.5% by the end of the year.

Second, economic activity is stalling. The UK economy has made a lot of progress in recent months and has recovered to about 1% below its pre-pandemic crisis peak. But in July, GDP barely moved. Over the past few weeks, labour and product shortages have been more pronounced and the fuel crisis has made matters worse. With businesses unable to get fuel in their vans and lorries, the prospect of a stagnating economy has increased.

How does this compare to the stagflation of the 1970s?

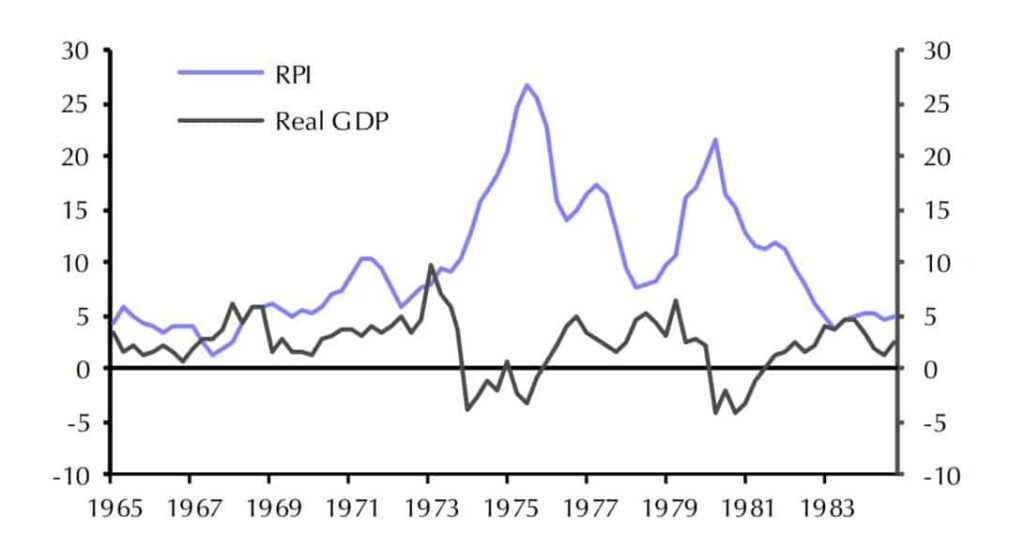

If the 1970s was ‘proper’ stagflation, then we are experiencing stagflation ‘lite’. The below chart puts it into perspective. The blue line shows that during the 1970s the RPI measure of inflation rose to over 25%. It also shows, as depicted by the black line, that GDP growth fell below zero on a number of occasions, as the economy moved in and out of recession. At the moment, inflation is around 4–5% and GDP growth is at zero, suggesting that this is more of a whiff of stagflation than the real deal experienced during the 1970s.

Source: Refinitiv, Capital Economics

Could this bout of stagflation become more serious?

The big factors that brought inflation down in the 1980s and the 1990s were globalisation and changing demographics. Labour became cheaper (in China, for example) and rapidly growing populations meant there were more people able to work. But while the effects of these two structural dynamics are fading, the emergence of technology (reinforced during the pandemic) and a more flexible workforce are very strong forces to keep inflation lower. This leads us to believe that we are still in a low inflation environment. And so while inflation may rise over the next six months or so, we believe it will fall back to around 2%.

Do you think interest rates will rise?

The US Federal Reserve has indicated that it is happy to allow inflation to stay above its 2% target, but the Bank of England has emphasised that the inflation target of 2% applies at all times. And if there is one thing that keeps central bankers up at night, it is worrying about inflation expectations – and there are signs that investors are expecting higher inflation. When inflation rises (and looks like it will stay high), central bankers jump out of their beds and start pulling the interest rate trigger.

With inflation rising to around 4–5%, we believe interest rate hikes are coming, but we don’t think they will rise very fast or very high. We’ve pencilled in an interest rate increase from 0.1% now to 0.25% in May next year, followed by another increase in 2023 before rising to its pre-pandemic level of 0.75% in early 2024.

Do you think the UK economy will recover faster than many are predicting?

We are in the optimists’ camp. We believe that the UK will get back to a situation where the economy is growing at a decent clip and be pretty close to pre-pandemic trends by sometime in 2023. We also believe that the economy can actually grow at a faster rate without generating too much inflation. The message from us is, we’re in for a bit of a bumpy ride over the next six months or so, but let’s not write-off the UK economy for the next three or four years. It will do just fine.

What does this mean for financial markets?

The movements in financial markets lately demonstrate that people are worrying. No or little economic growth and higher inflation are not a great combination for either equities or bonds. Global equity markets didn’t move much during the third quarter and they have fallen back recently, partly because of the weaker outlook with corporate earnings unlikely to be as high as previously thought.

But while we expect markets to be uncertain for the next few months, based on our forecasts that inflation will start to fall back next year and the economy will start growing again, we expect this uncertainty to be temporary. As we get into the second half of 2022, we believe equity prices will climb higher, although not at the same pace as they did in the decade leading up to the pandemic.

Will property prices continue to rise?

We think that house price inflation will slow next year from around 10% to about 5%. But we’re not expecting an outright fall in prices, neither are we expecting the fast slowdown that some expect. We expect the market to be propped up for longer by a structural change that has been triggered by the pandemic where people want more space and are willing to pay more for it.

What does it mean for Weatherbys Private Bank clients?

At Weatherbys we build portfolios that make sense for the long-term objectives of our clients. Our portfolio construction is cognisant of ongoing economic conditions and the structure of the economy. If that structure changes, for example if inflation does start to become a problem, we consider adjusting portfolios in response to that new reality or discuss with clients as to whether their investment profile is still appropriate or needs changing. We have started using an assumption of elevated levels of inflation in our cash flow models for clients to see what that scenario would mean for them, and to give us the chance to recommend changes to their investments if appropriate.

We continue to believe that equities provide the best protection from inflation over the longer-term. There is no investment asset that reliably protects against inflation in the short term, but many studies highlight that equities tend to outpace inflation over the long term. However, it’s important to be aware that not all equities are the same, and depending on the environment, some stocks will fare better than others. Prices of high-quality bonds can rise during periods of deflation and so can offer some protection against falling prices.

The overriding message is to stay diversified and balanced in your investment portfolio. And you may wish to consider to take a step up the risk ladder by investing, because staying in the perceived safety of cash is a risk even when inflation remains subdued.

Important information:

Investments can go up and down in value and you may not get back the full amount originally invested.