With the resignation of Sir Keir Starmer as Prime Minister, the door to Number 10 Downing Street has been unlocked for his Mancunian pretender, Andy Burnham. The latter has ignited hopes among Labour MPs that, at long last, spending on the public sector might be increased.

Burnham is well known for insisting that, “We’ve got to get beyond this thing of being in hock to the bond markets.” He was not, however, advocating for spending within the national means and paying down the public debt.

Rather, his focus seems to be on nationalising utilities and large-scale council house construction, funded by higher taxation.

Robbing Peter to pay Paul

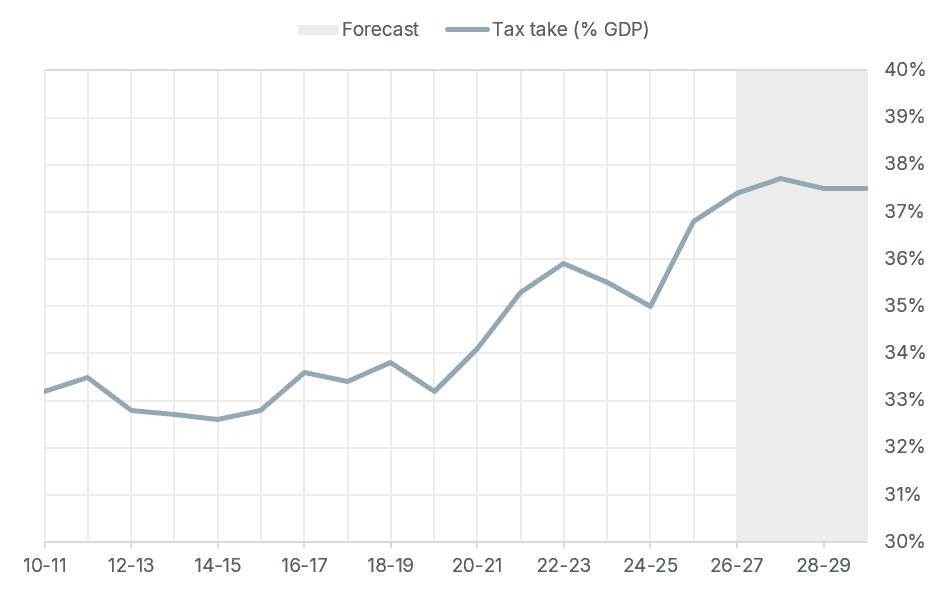

The tax take is the highest it has been since records began in 1948. But curiously enough, this has happened despite the median earner paying out roughly the same proportion of their gross salary.

This is partly because of the rising personal allowance, and partly because income tax rates and employee National Insurance contributions have remained broadly constant.

Instead, it is the wealthy (or supposedly well-off) who have shouldered the burden: pensions have been stripped of their reliefs, the additional rate threshold has been lowered from £150k to £125k, dividends and capital gains taxes have increased, small businesses pay more in employer National Insurance contributions, private school fees are now subject to VAT, and of course family farms now face ruinous inheritance taxes.

Burnham’s inner circle seems to want more of the same.

Among other ideas apparently being toyed with, Burnham’s advisers are said to favour hiking National Insurance contributions on higher earnings and equalising tax rates on capital gains and income.

Until the pips squeak

The trouble is that Labour is running out of ‘others’ to tax. At some indiscernible point, the government takes a greater share of a diminishing sum.

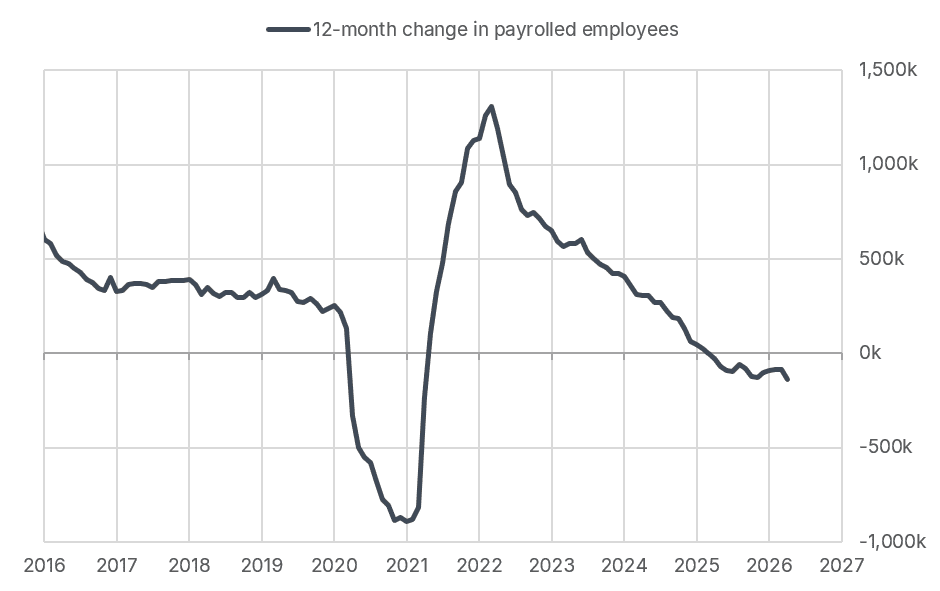

For instance, the steady drop in the number of employees on the collective payroll – to below pre-Covid levels – can be explained at least in part by Rachel Reeves’ decision to make it more expensive to hire workers. Any further squeeze on incomes could well exacerbate the situation.

Similarly, it is plausible that higher rates of capital gains tax could stifle entrepreneurial activity, leading to an overall drop in revenues for the Exchequer.

All this comes at a time when the UK faces the highest energy costs in Europe. Running a data centre costs roughly two to four times as much as it does in the US, and the regulatory burden is considerably higher than it is across the pond, too. These are self-imposed wounds – and the less said about manufacturing competitiveness compared to China, the better.

Indeed, in the latest economic temperature checks (surveys of company managers who make purchasing decisions), the British service sector seems to be contracting, while its American cousin is more ebullient.

On borrowed time

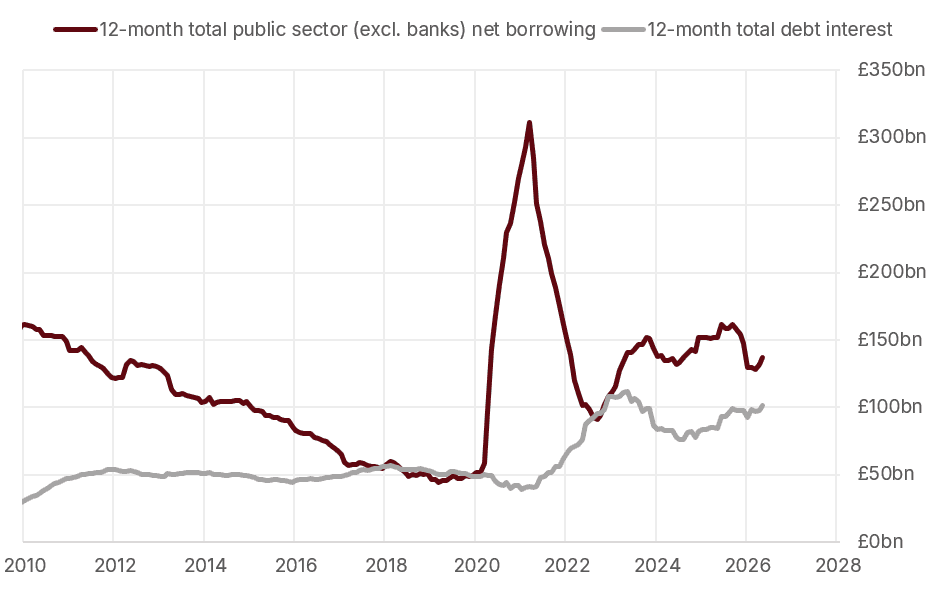

The fiscal reality is that public sector net borrowing is uncomfortably high, standing at £23bn in both April and May this year. Meanwhile, debt interest was almost £12bn in May alone, and over £100bn in total over the past 12 months.

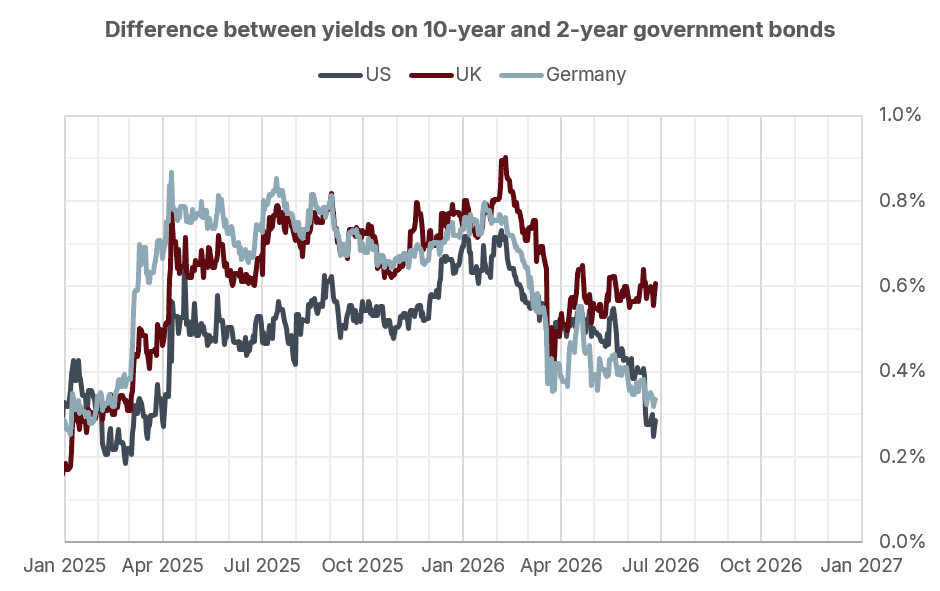

And while Andy Burnham might not want to pay much attention to bond markets, bond markets are very much paying attention to him.

The difference between 2-year and 10-year government bond yields is an expression of how much extra lenders demand for taking on the fiscal risk of longer-term debt – and it is now markedly higher in Britain than in the US or Germany.

While the trend has been uncomfortably upwards for some time now, there was a pronounced spike in this long-term lending premium after the Makerfield by-election. The verdict of bond investors seems clear.

Some commentators have even floated the possibility of another IMF bailout, should things continue on their present trajectory. It is worth emphasising that the UK’s previous experience of this unhappy outcome in 1976 was born of an imbalance of payments: we had to borrow dollars to stabilise sterling.

Today’s predicament has similar political causes to those which landed us in the mire of the 1970s, but is different in important ways. Now, it is unlikely that the IMF would even have the funds to be able to dig Britain out of trouble (or, for that matter, France, which is arguably in an even worse state).

It remains very much within our gift to course-correct – to bring public spending back on an even keel. As such, some sort of debt meltdown is far from inevitable – but it is all too uncomfortably plausible.

Bond villains

The worry is not just that we will end up paying more in debt interest – indeed, we’ll increasingly have to borrow more just to service it – but that the character of the government bond market is changing.

Whereas British government bonds – ‘gilts’ – were once almost the preserve of low-octane pension funds, who bought them to hedge their defined benefit liabilities, the landscape is now the hunting ground of profit-seeking fund managers with a licence to make a killing.

The latter are far more sensitive to prices than the former, and far more skittish too. As such, the Debt Management Office (DMO) much prefers, wherever possible, to borrow from old stalwarts with skin in the national economic game.

But as the size of the Bank of England’s balance sheet has ballooned, and defined benefit pension schemes have started to die out in favour of defined contribution alternatives, the DMO has had to rely more on the kindness of avaricious strangers.

There is an unwelcome ‘latent heat’ nature to this transition: it may seem that, as long as gilt auctions are successful, all is well. But the very act of having to ask for a morsel more from pure profit-seekers could provoke these more discerning buyers into demanding even higher yields.

In other words, the cost of national borrowing could rise slowly, and then very quickly.

The bigger picture

For investors in shares of companies around the world, the British stock market is unfortunately a shadow of its former self, representing only about 3% of the total value.

As such, the ructions in Westminster are more or less inconsequential when it comes to the share prices of a well-diversified portfolio.

However, there are ways in which this political upheaval could nonetheless have outsized influence. After all, it wasn’t just bond prices that sold off after Makerfield – the pound did, too.

To put it another way, the dollar strengthened, and so shares in US companies became relatively more valuable to a sterling-based investor.

This may well come as cold comfort, though, to those who strive to play positive-sum games in a country whose government seems to prefer net zero.

About William Morris

William is Head of Investments at Weatherbys Private Bank. He has over a decade of experience encompassing investment advice, portfolio optimisation and risk modelling, and enjoys bringing this world to life in a friendly and engaging way.

What you need to know

Investments can go up and down in value and you may not get back the full amount originally invested. Past performance is not a guide to future performance.