Properties in the outer suburbs of Greater London have experienced significant price growth over the past two years as they benefited from a change in buyer preference and the ‘race for space’ during the height of the pandemic.

Buyers wanted more space amid the restrictions and also were able to capitalise on the Stamp Duty Land Tax (SDLT) holiday for lower value properties. Transaction volumes increased as buyers rushed to capitalise on up to £15,000 in SDLT savings, which were available until the end of June 2021. Data from the HM Land Registry from July 2021 is not yet available, though it is likely volumes dropped during the month as sales are typically brought forward when tax changes are implemented.

However, Prime Central London (PCL) did not experience anywhere near the same price growth as proximity to places of work and the vibrancy of London became less relevant during lockdowns and a period of restrictions. During the first 12 months of the pandemic, prices in PCL dipped before recovering in the second half of 2021.

Demand for larger properties meant that prices for houses outperformed flats by 3.9 per cent over the two years – significantly, overseas buyers were largely absent. Indeed, capital values in central London have only just recovered in recent months to just below the level they were two years ago (−1.2 per cent).

Is opportunity knocking on PCL’s door?

This divergence in price growth between houses and apartments has created an opportunity for those renewing their interest in acquiring PCL property. The data suggests there was a ‘stepped’ increase in values for those properties that had a garden or outside space; this factor alone attracted a 7 per cent premium in June 2020, compared to 5 per cent before the pandemic.

The political uncertainties of recent years, namely Brexit, culminating in the fallout from Covid-19, have caused prices in the central areas of London to cool. A nascent recovery is possibly being witnessed, with overall prices for the market over the December 2021 quarter increasing by 1.6 per cent, although not all market segments have behaved in unison. The positive sign witnessed in recent months is best reflected in the heatmap below.

Demand for apartments is starting to increase, as many young professionals returning to the capital are looking for small, competitively priced units. Savvy UK-based buyers and tenants are taking advantage of the absence of overseas competition, not all of whom have yet returned to London.

Buyers and tenants are back, as life returns to normal

There is now a trend for buyers to forgo space to acquire smaller properties with a far more central and prestigious address than they would until recently have been able to afford. With the lifting of all Covid restrictions, those who did move out of London during the pandemic are now looking for a central and conveniently positioned pied-à-terre to overnight their two or three days spent in the office. These buyers want small but conveniently located apartments that they can ‘lock up and leave’ when returning home for the weekend.

This opportunity within the apartment sales market will close once the inevitable return of overseas buyers gets underway, as has already been witnessed within the lettings market. Tenants who are expecting to remain within the UK for an extended period have been the first to return. Buyers have waited for more global restrictions to lift.

To fully understand the central London residential market, it is important to consider transaction volumes alongside price movements. The nature of central London residential property ownership is such that at times of deflated pricing, owners become less inclined to sell – it is rare to encounter distressed sellers.

As a buyer, it is helpful to understand that stock levels are far from abundant and will only improve when price increases are triggered by overseas demand. Anyone entering this market should be cognisant that while choice may not be plentiful, increased supply will accompany increased prices. In short, a delay will not necessarily improve the outcome.

A repeat of the ‘Boris Bounce’?

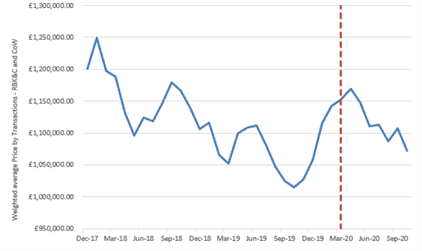

With the anticipated return of overseas buyers, PCL properties are set for an overdue period of price growth, similar to that witnessed in December 2019 when a sharp price increase followed the general election – the so-called ‘Boris Bounce’.

Investors and house movers alike took comfort in the clear direction of travel the general election result provided. If not for the pandemic, this short period of growth could have extended into a significant recovery. Naturally, we can only reliably call either the top or bottom of a market with the benefit of hindsight. However, the data suggests we can make a call within the central London flats market.

About London Central Portfolio (LCP)

LCP is a boutique sized private client buying agency. Founded in 1990, LCP provides access to buying opportunities as well as project management and design solutions to suit all aspirations and budgets for UK and overseas property investors and homebuyers seeking exclusive prime London real estate.

Sources: LCP in-house analysis of Bricks and Logic data and HM Land Registry HPI for PCL (Royal Borough of Kensington & Chelsea (RBK&C) and City of Westminster (CoW)

Important information:

These views are solely the opinions of London Central Portfolio, an independent property advisor, and do not necessarily reflect the views of Weatherbys Private Bank.