This has become a favoured tool of Chancellors looking for ways to raise revenue. Inflation tends to lift wages and the price of assets. If tax allowances are not raised in line with inflation too, more people find themselves paying higher taxes. Research by Weatherbys has demonstrated the impacts1.

IHT freeze costing some families over £300k

- The cost of IHT freezes to the estates of couples with over £1.4m is over £177,000

- For wealthier couples it is £305,000

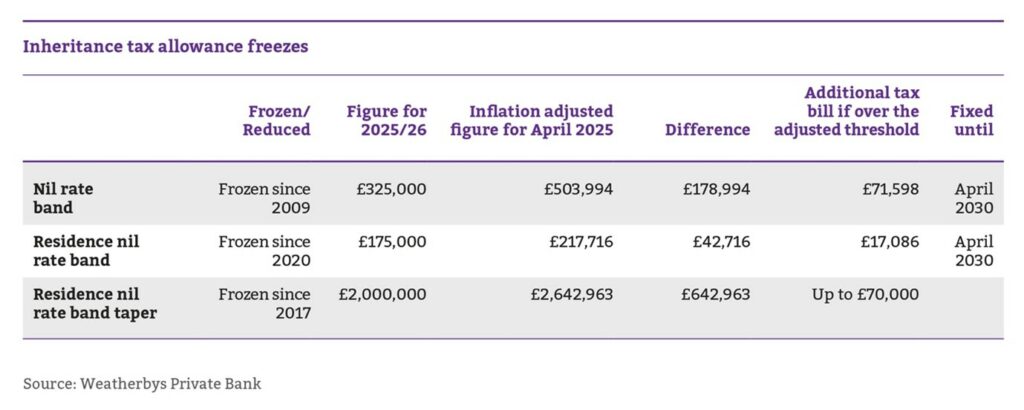

The biggest impact of tax freezes has been on the IHT nil-rate band. This has been unchanged, at £325,000, since 2009. Had it risen in line with inflation it would now be nearly £504,000. The freeze is set to be in place till at least April 20301.

The residence nil-rate band has not changed since it was set at £175,000 in 2020. Had this risen in line with inflation it would now be nearly £218,000. Back in 2009 IHT raised around £2.35bn. The OBR estimates IHT receipts will hit £14.3bn in 2029/30. Around £1.5bn of this will come as a result of the Chancellor scrapping IHT exemption on pension assets3.

The consequence of these two IHT tax exemption freezes on a couple’s estate over £1.4 million is a hike of over £177,000 in their tax liability.

Wealthier families are hit even harder, because the residence nil-rate band taper has been held at £2m since 2017. For every £2 of assets held over this £2m an estate loses £1 of IHT nil-rate band allowance. Had the taper threshold risen in line with inflation it would be £2,642,963.

Add in the other freezes and a wealthy couple with an estate over £2.64m face £305,000 extra in IHT liabilities. Removing the IHT exemption on pensions means many more families are now in this bracket and may not have realised.

The fact that pension savings are to be included in people’s estates for IHT from April 2027, means that many more families will find themselves in this position than before and in need of IHT planning advice.

Clare Munro, Senior Tax Adviser at Weatherbys Private Bank, said: “The government actually has to pass primary legislation each year to prevent income tax thresholds rising with inflation. Despite this a series of Chancellors has used tax allowance freezes as a way to raise revenue without many noticing and without grabbing nasty headlines. Now, though, those freezes are beginning to hurt people at all levels. People are noticing the impact in their pay packets, and many families are going to start noticing the impact in any inheritances they receive.

“IHT is a hated tax already. People see it as a tax on money that’s already been taxed, and to find the government taking an extra £300,000 or more through allowance freezes will be painful.”

Income tax threshold freezes and allowance reductions costing high earners nearly £9k a year

- Anyone earning £150,000 is paying £9,472 extra

- Anyone earning £125,140 is paying £8,229 extra

- Middle income earners on £63,075 are paying £3,201 extra

- Basic-rate taxpayers earning over £15,769 are paying £640 extra

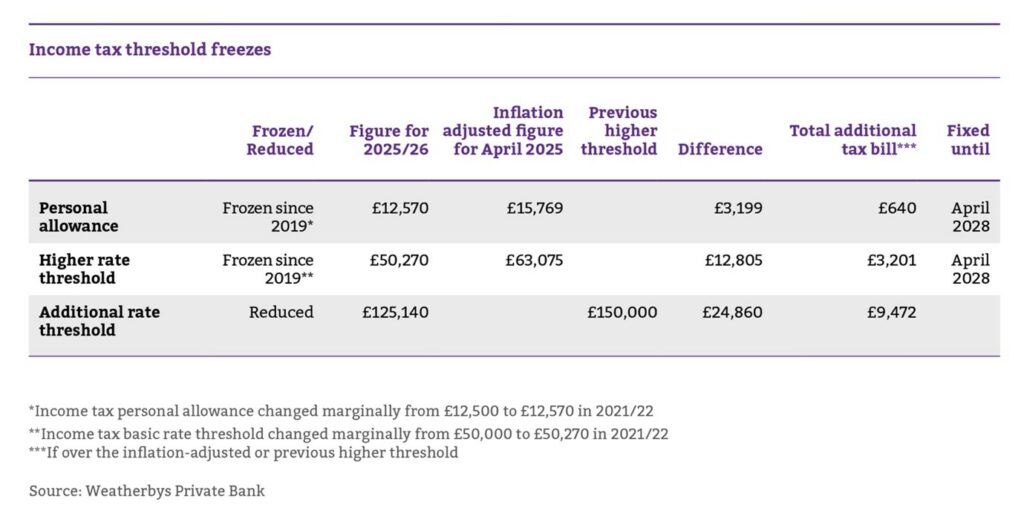

The other big impact on freezes is on income tax thresholds. The personal allowance, at £12,570, and basic-rate upper threshold, at £50,270, are effectively unchanged since 2019. If they had risen in line with inflation they would now be £15,769 and £63,075.

In April last year the threshold for the 45% additional-rate income tax was reduced from £150,000 to £125,140. This has hit high earners and comes on top of hikes across all tax bands.

Meanwhile, more people are now caught by the 60% marginal rate of tax that hits those who earn between £100,000 and £125,140, as a result of a relief taper that means for every £2 you earn over £100,000 you lose £1 of your personal allowance. If this had risen in line with inflation it would now be nearly £152,000.

The consequence is that anyone earning £150,000 is paying £9,472 extra. Those earning £125,140 are paying £8,229 extra. Middle income earners on £63,075 are paying £3,201 extra and the cost even for basic-rate taxpayers can run to hundreds of pounds. Basic-rate taxpayers earning over £15,769 are paying £640 extra.

Clare Munro said: “This is a frankly illogical tax. I’m not a fan of tapers anyway, but had it risen in line with inflation it would only kick in for those earning over £151,885. It means we have an effective income tax rate that goes from 20% to 40% to 60% and then 45%. This taper freeze alone is costing some people over £5,000 a year in income tax, and it’s probably causing many people whose earnings are in this region to cut their hours – thereby reducing our productivity and costing tax revenue.”

She added: “Our research shows that tax allowance freezes are affecting everyone. It’s almost impossible to escape their impact.”

Other freezes hitting graduates and those with capital gains

Many graduates paying £500 more p.a.

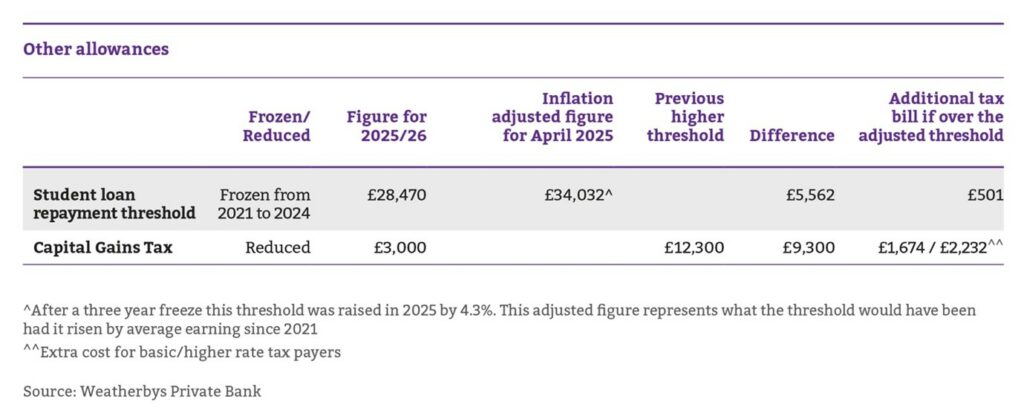

The student loan repayment threshold for those on the Plan 2 scheme was lifted to £28,470 in April 2025 after three years on ice. But that 4.3% increase did not make up for lost ground. Had the threshold been lifted in line with average earnings since 2021 graduates would not be liable to pay the 9% student loans tax until they were earning £34,032. This tax freeze is costing those graduates earning over that figure an extra £501 a year in loan repayments.

CGT allowance freezes costing many over £2,000

Someone with a capital gain of £12,300 or more now pays £2,232 extra tax if they are a higher-rate taxpayer or £1,674 if they are a basic-rate taxpayer, as the allowance was shrunk from £12,300 to £6,000 in 2023/24 and then to £3,000 from April last year.

Clare Munro said: “When the rate was higher it gave many couples the chance to share a decent allowance and, through careful ongoing management, mitigate and often eliminate the issue of CGT. An increasing number will find themselves caught not just having to pay this tax but also with the tax return hassle it brings.”

What you need to know

Tax laws may change and taxation will vary depending on your own personal circumstances.

1 We have used the annual CPIH from the previous calendar year to calculate an inflation-adjusted threshold for each April.

2 https://obr.uk/forecasts-in-depth/tax-by-tax-spend-by-spend/inheritance-tax/