We know we need to pay the taxes that are legally due, but the way you structure your retirement income can make a big difference to the tax bill. And, as any tax saving feeds directly into your bank account, it can improve the quality of your retirement. The recipe for success is to use the attributes of different investment pots to your advantage.

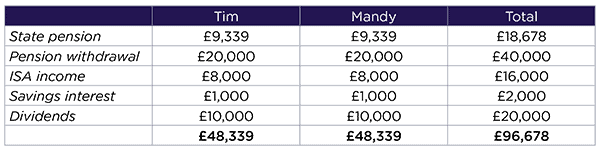

Looking at how this might work, let’s take husband and wife couple Tim and Mandy as an example. They each have £500k pension pots, £200k in equity ISAs and £100k in savings accounts and £300k in general investment accounts. As they retire, we could build up their income:

There are several ways to draw down on a pension, but Tim and Mandy choose to take a series of lump sums or Uncrystallised Funds Pension Lump Sums or UFPLS’s, of which the first 25% will usually be tax free. Their ISA income will always be free of income tax, and any gains on the ISA investments will not bear capital gains tax. For basic-rate taxpayers, savings interest is eligible for a £1000 0% savings allowance and dividends are also eligible for a £2,000 tax free allowance, with the balance being taxable at 7.5%.

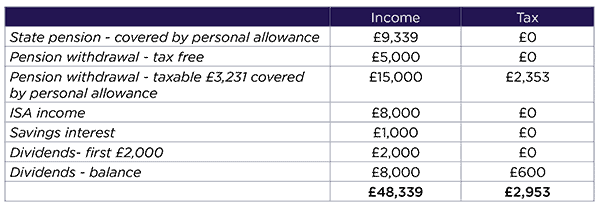

The tax result for Tim looks like this:

Of course, the result for Mandy is identical, so this structure allows the couple to take a joint income of over £96,000 with tax of £5,906, simply by using the structures that are available to all of us. The effective tax rate is 6.1%.

That’s not necessarily the whole story either; if Tim and Mandy have shareholdings standing at a gain, they could realise more cash on a sale and use their £12,300 capital gains tax allowances to shelter the tax liability.

This happy result didn’t happen by accident though. It took some careful planning to ensure that the funds ended up in the right tax wrappers during the couple’s working lives so that the pots were ready to generate tax efficient income when they needed it. There’s nothing unduly complex about this strategy either and, if it generates sufficient funds for the couple’s lifestyle, it may well be all they ever need.

Important information

The value of an investment and its income can both increase and decrease and you may not get back the full amount originally invested. Tax laws are subject to change and taxation will vary depending on individual circumstances.